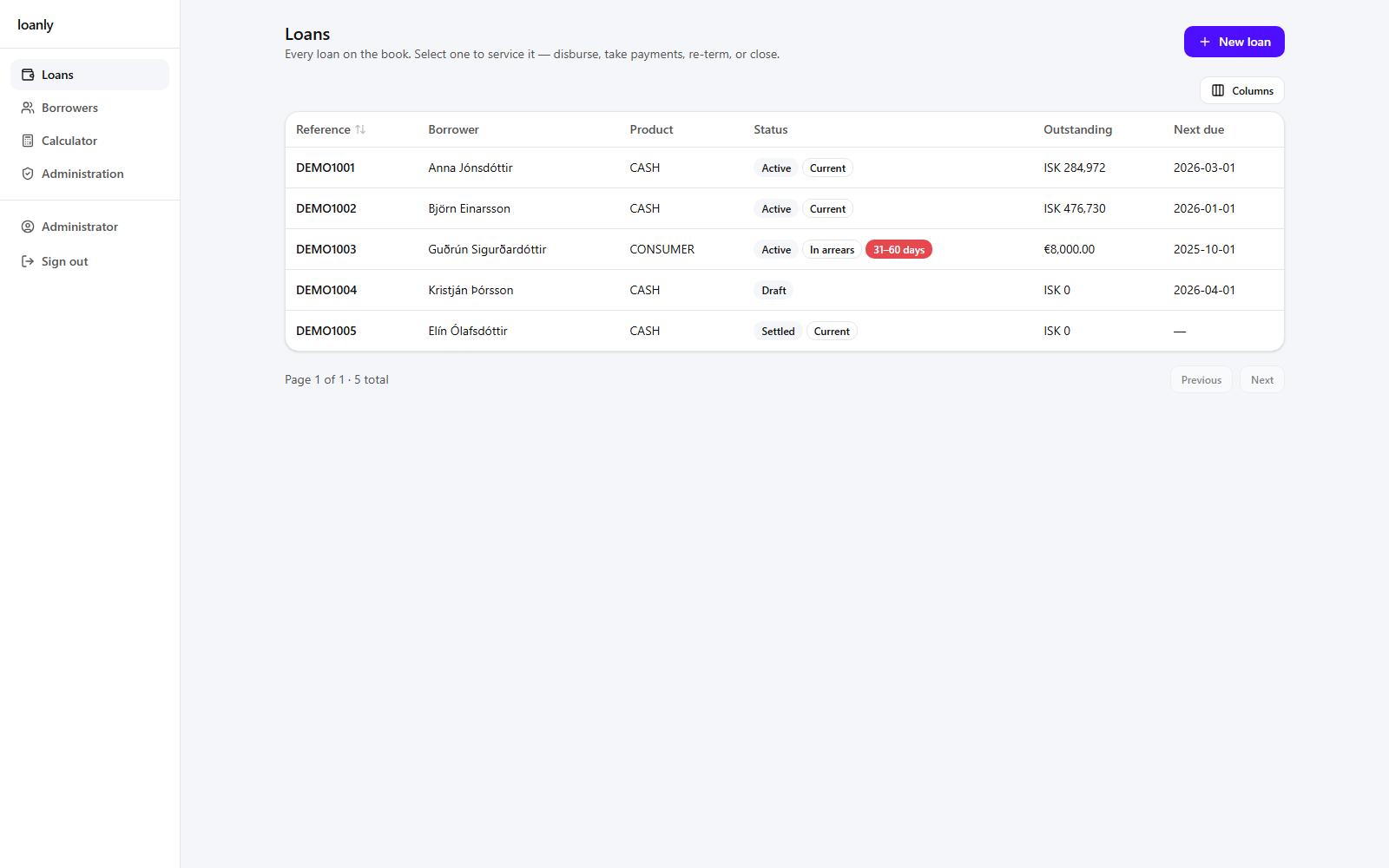

Loans

The loan book. Each row is a loan with its borrower, product, status, outstanding balance, and next due date. Create a new loan with New loan, or open one to service it.

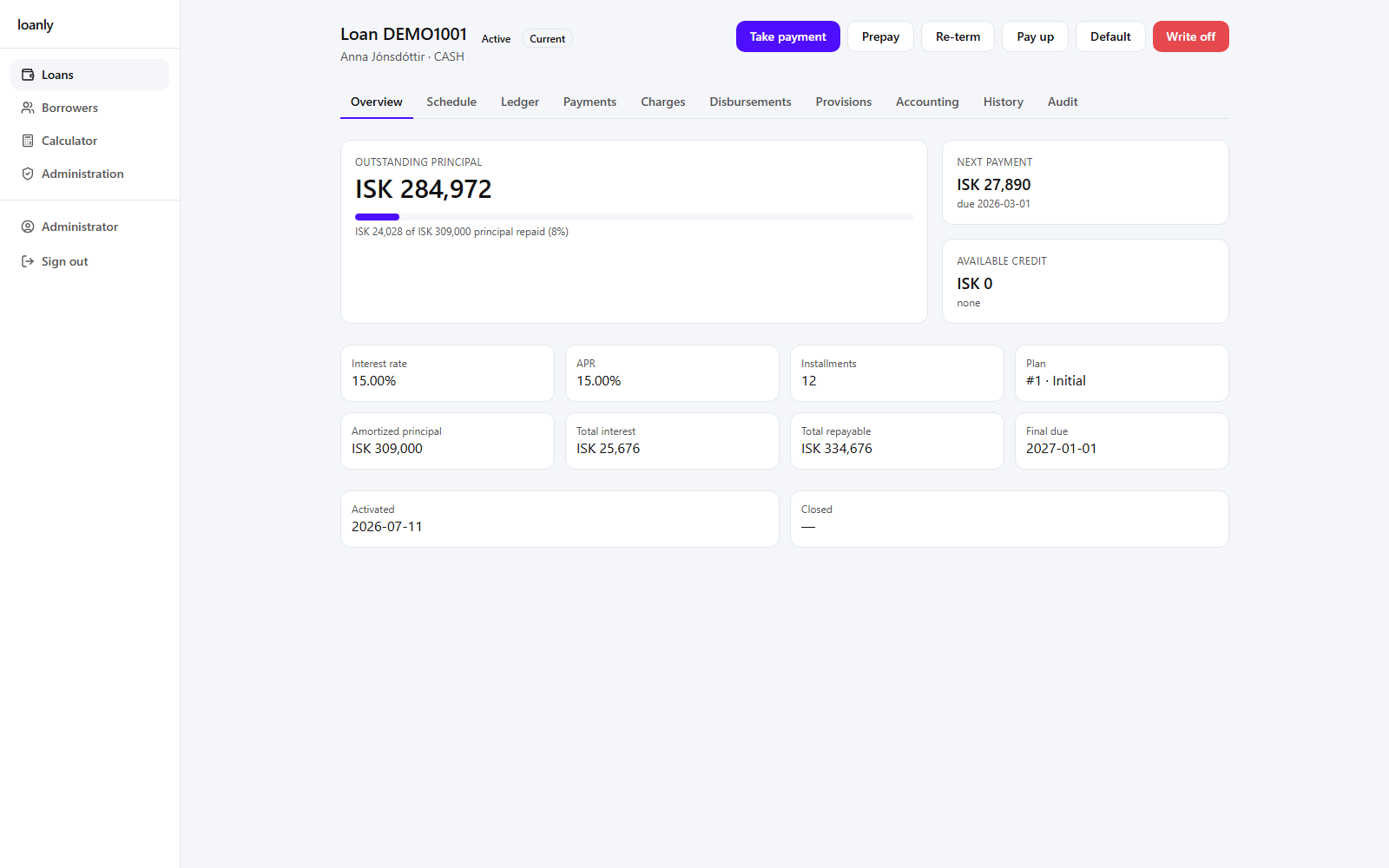

The loan detail

Opening a loan shows everything about it. The header carries the status and the servicing actions; below it, tabs break out the full history. Every tab is documented below.

Servicing actions

The buttons in the header drive the loan through its lifecycle (each is permission-gated):

- Take payment — record an incoming payment; it's applied through the waterfall (charges, interest, principal…).

- Prepay — an extra principal payment that re-amortizes the remaining schedule on the lower balance.

- Re-term — put the loan on a new schedule (new installment count and/or rate).

- Pay up — early settlement: quote the payoff figure as of a date, then settle and close the loan.

- Default / Write off — move a loan into default or write off the balance.

Tabs

Overview

Outstanding principal and repayment progress, the current terms (interest rate, APR, installments, totals), and key dates (activated, final due).

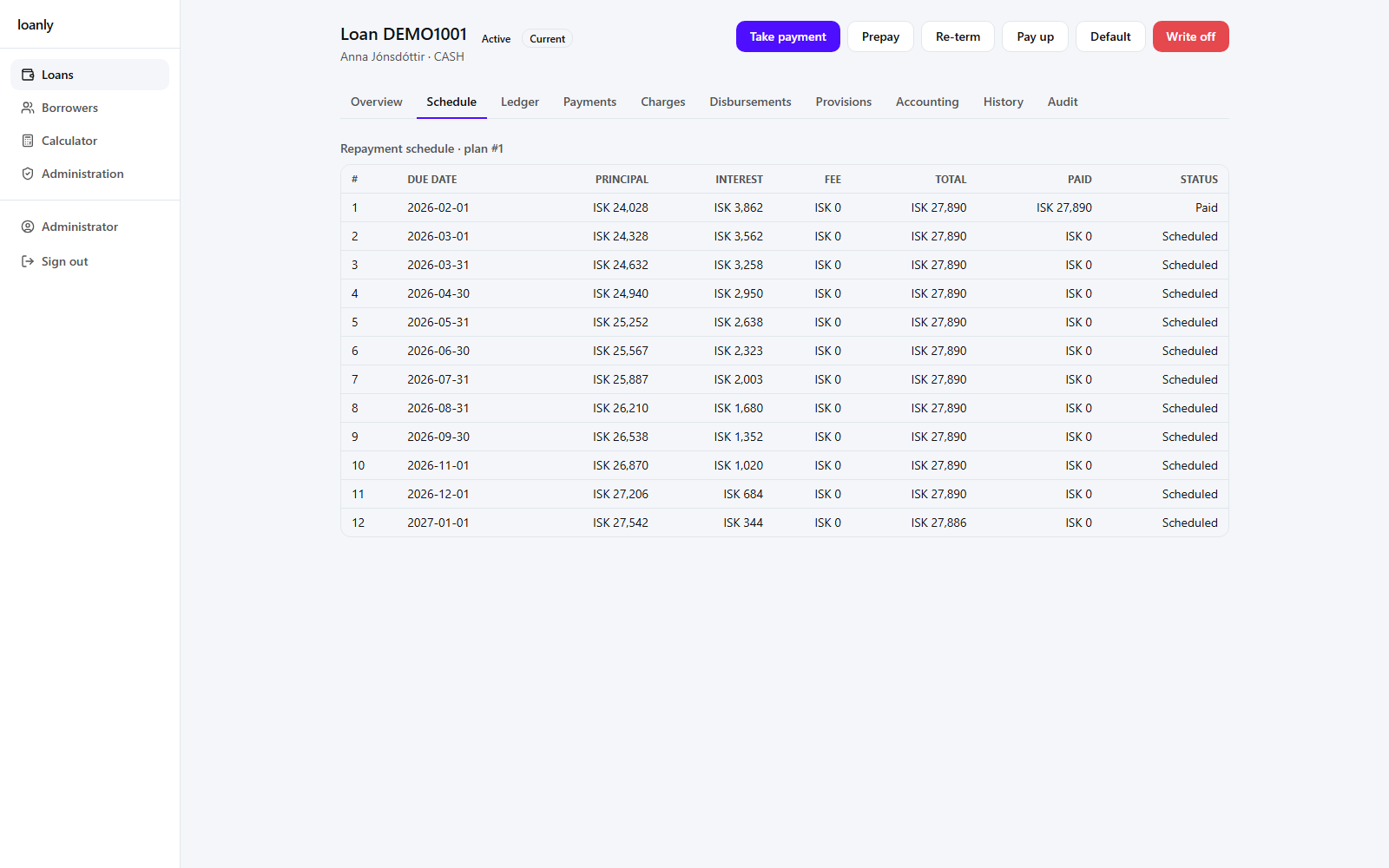

Schedule

The current installment plan — due date, principal, interest, fee, total, and paid amount per line, with each installment's status.

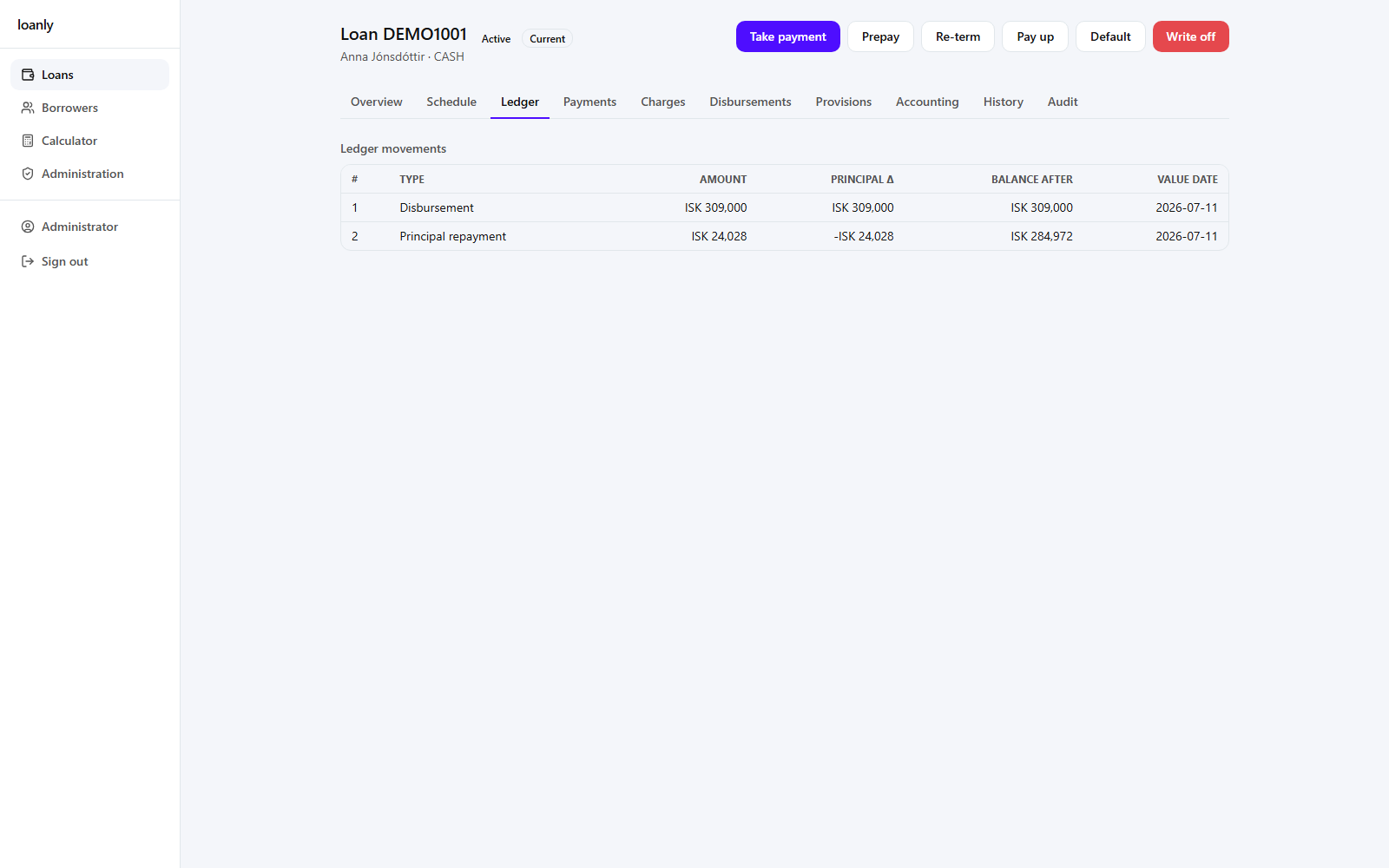

Ledger

The value-dated sub-ledger: every signed movement (disbursement, repayments) with the running outstanding balance. Append-only — the balance is the sum of the deltas.

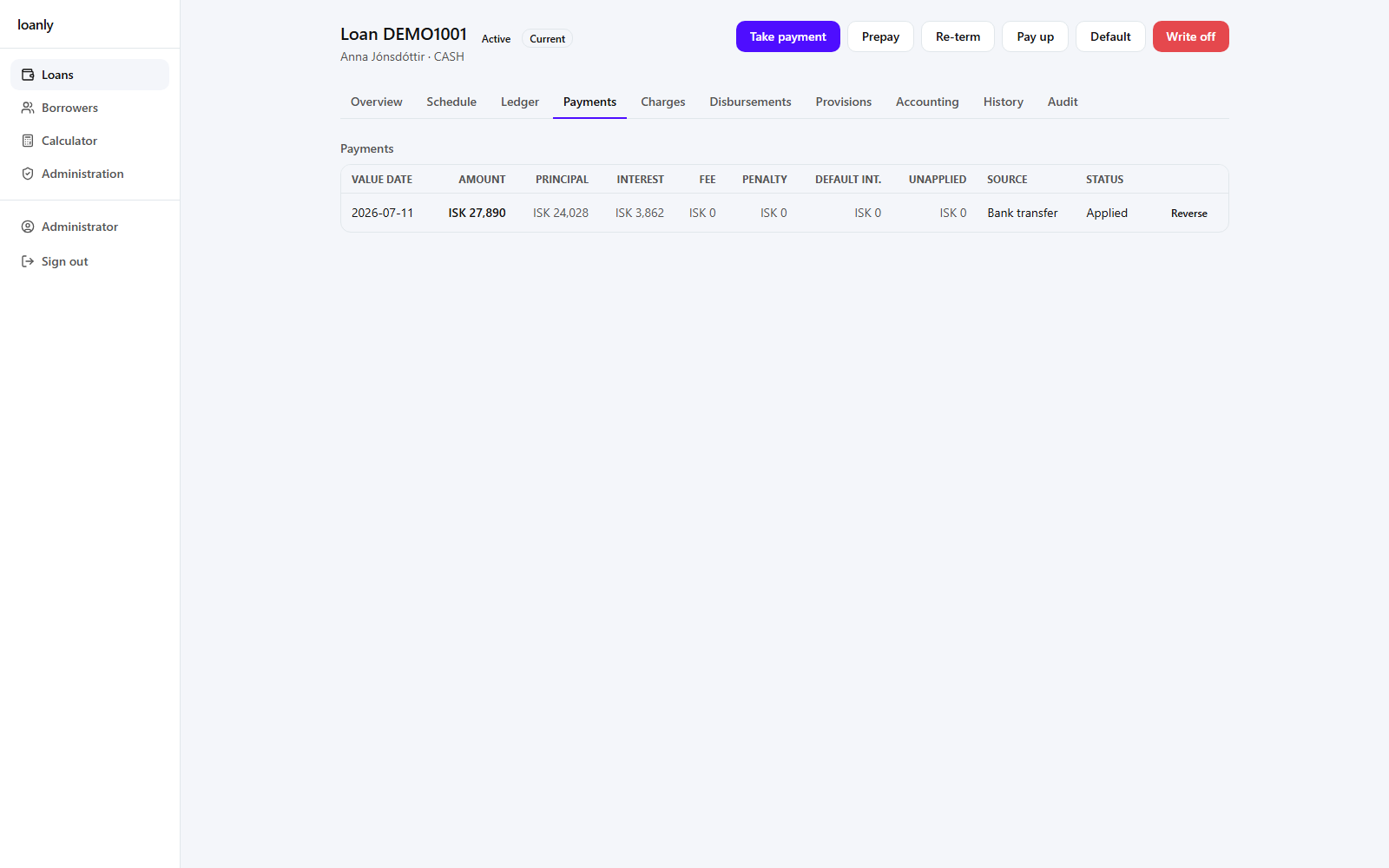

Payments

Recorded payments, each expandable to its allocation breakdown across principal / interest / fees / penalties / default interest, plus anything left unapplied.

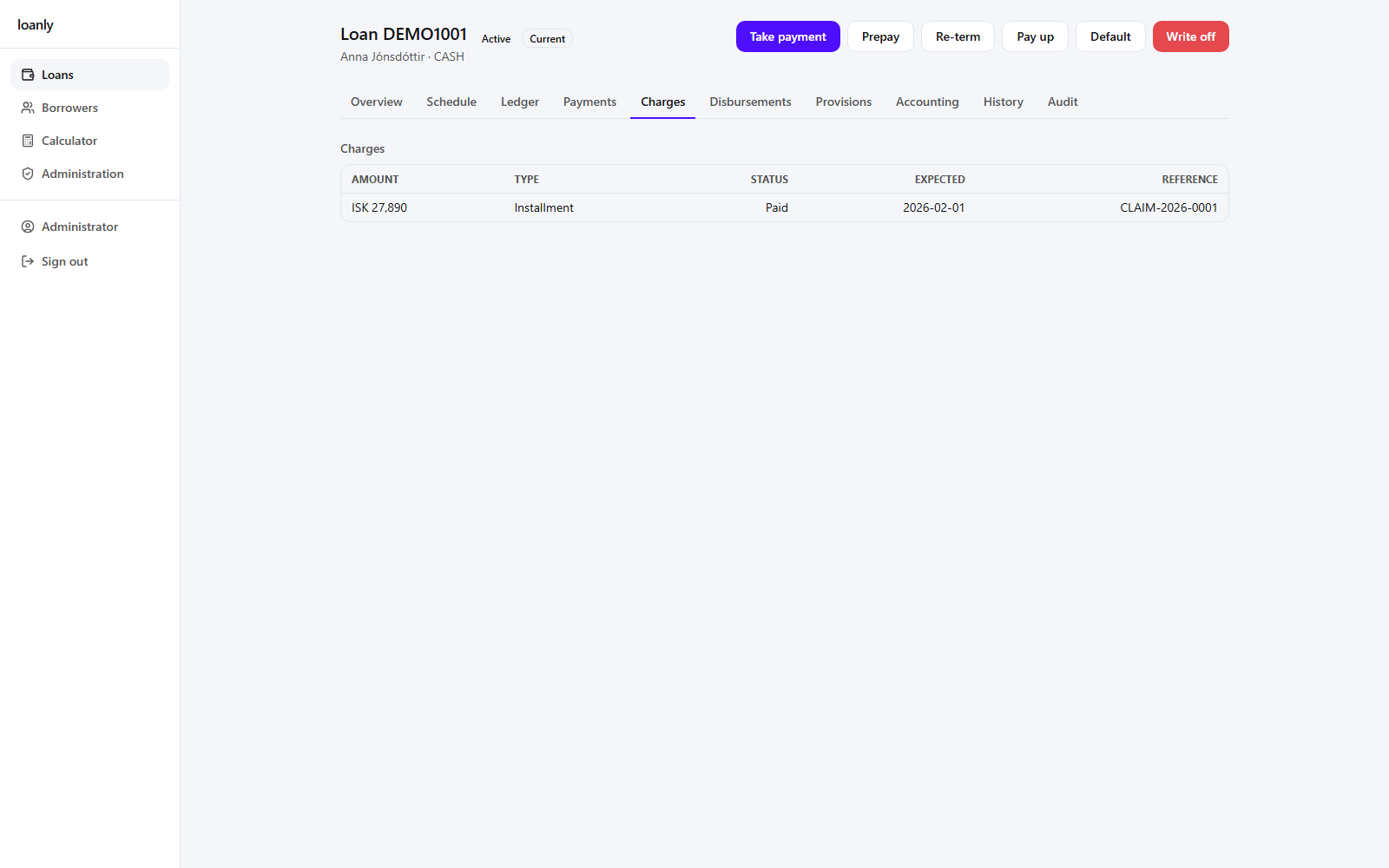

Charges

Collectibles raised against the loan (installment charges, additional-payment and pay-up charges, default costs), their status, expected payment date, and any bank-claim reference.

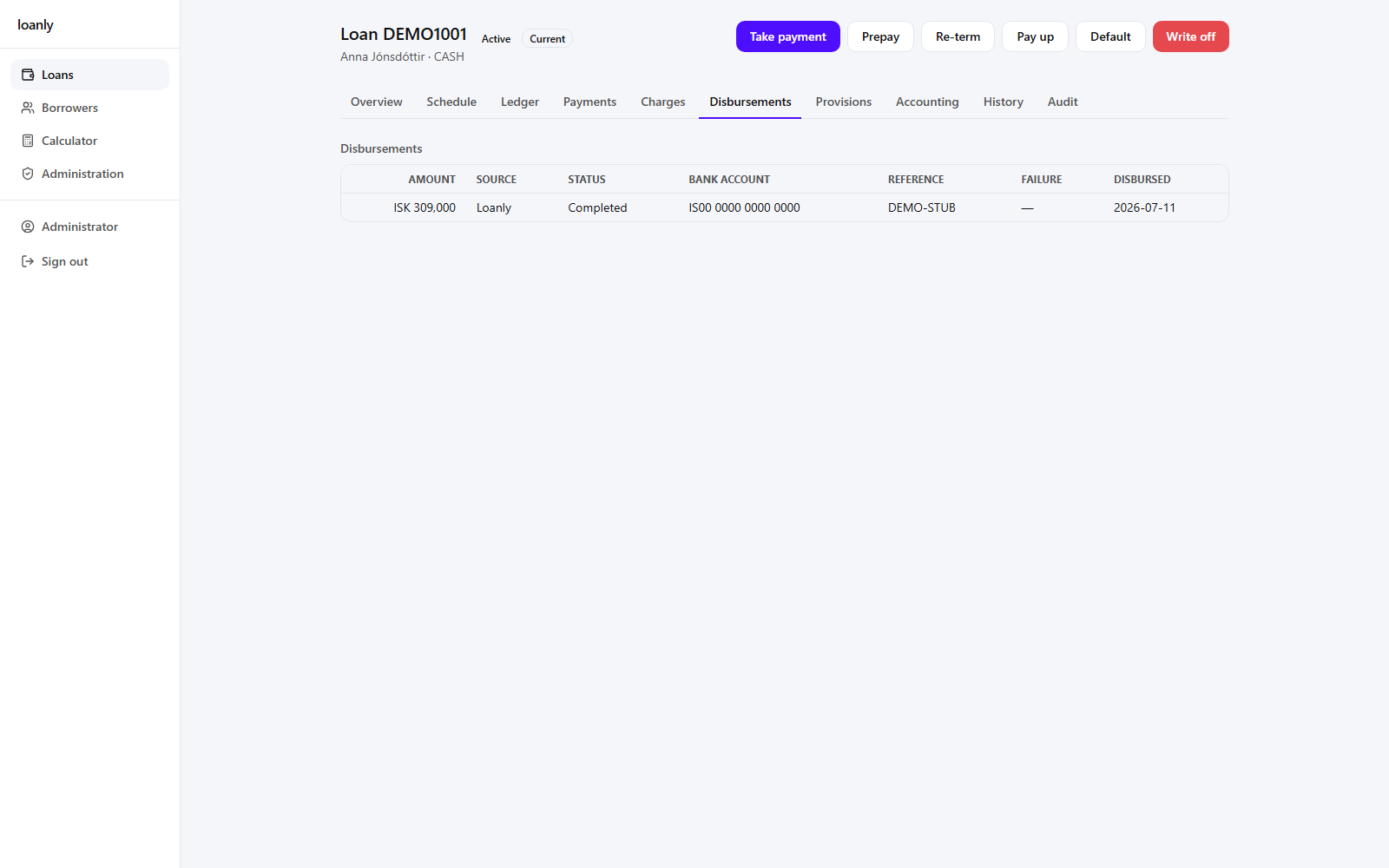

Disbursements

Payout records with their source (Loanly-performed vs partner-funded) and status (Pending → Completed / Failed), the destination account, the rail reference, and any failure reason. See Concepts → Disbursement.

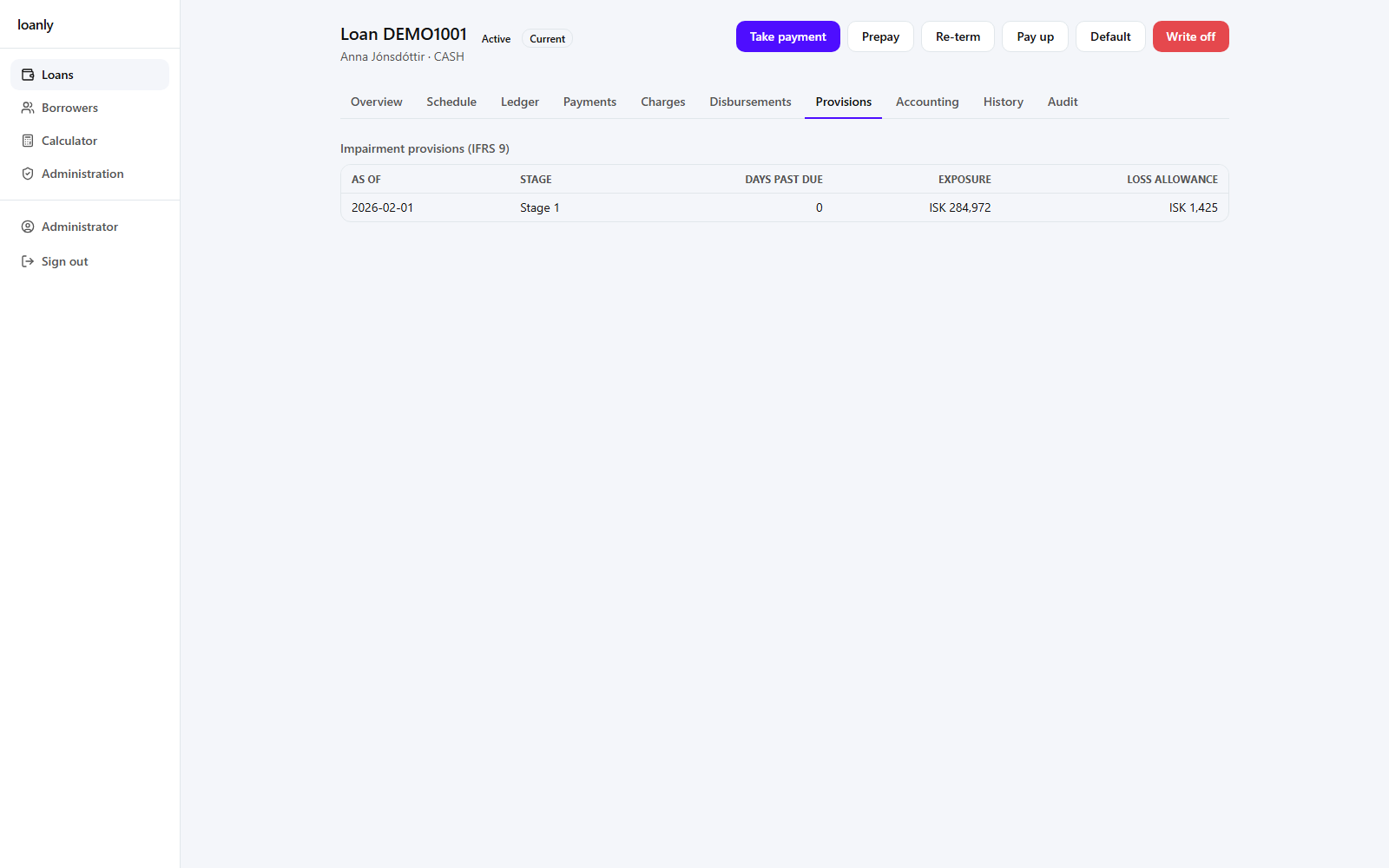

Provisions

IFRS-9 impairment snapshots per run date: stage, days past due, exposure at default, and the loss allowance.

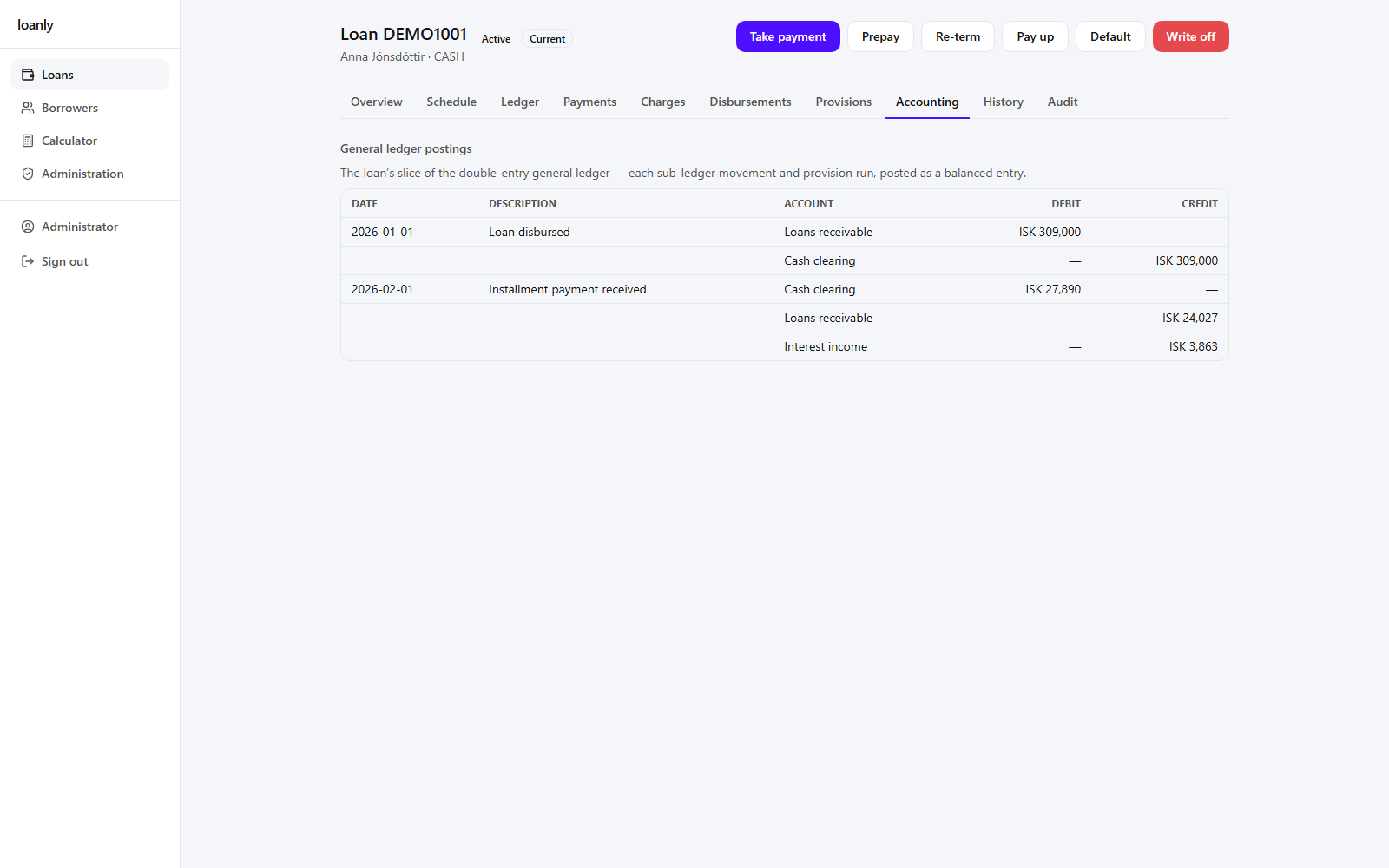

Accounting

The loan's slice of the double-entry general ledger — each sub-ledger movement and provision run, posted as a balanced journal entry.

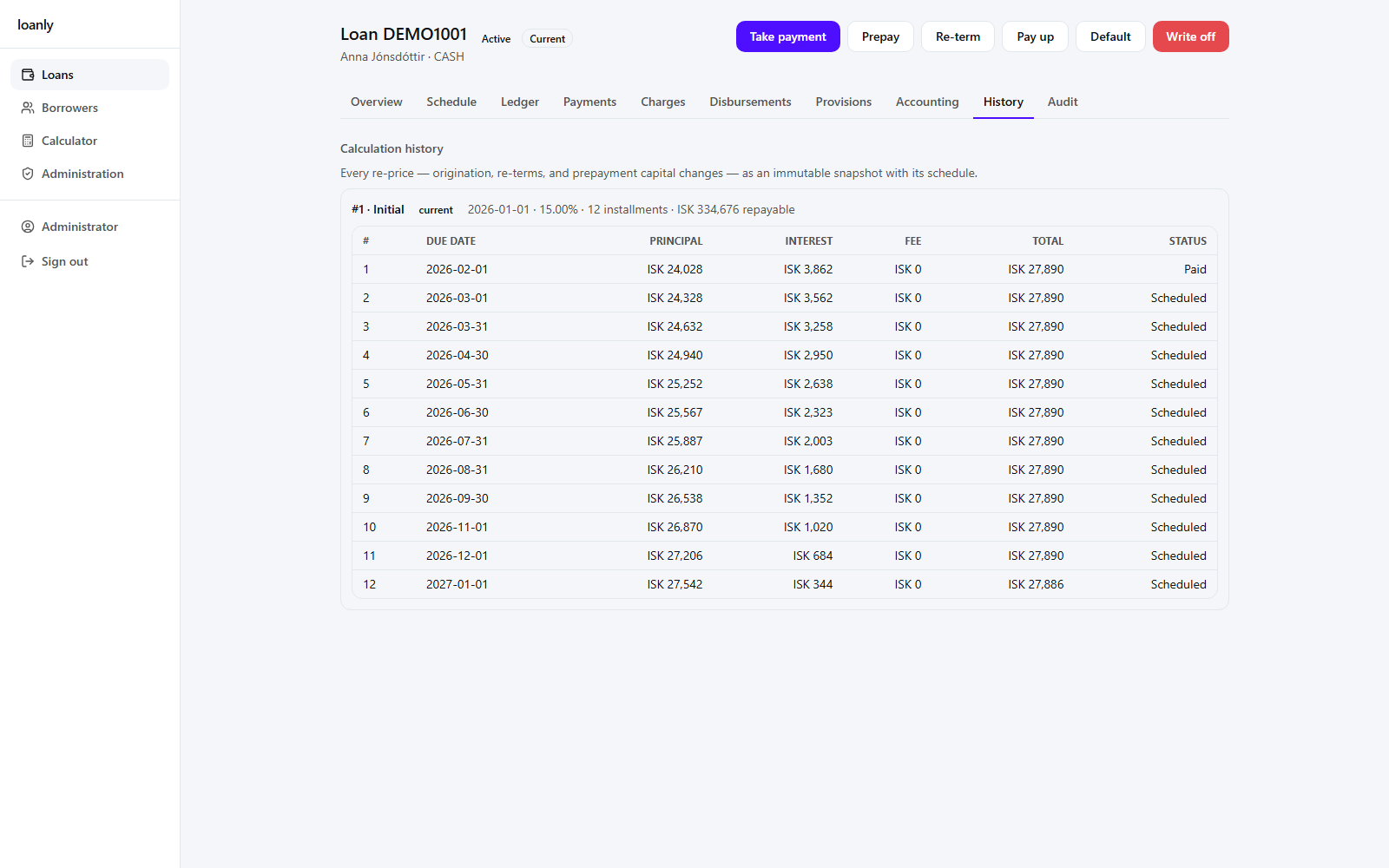

History

Every calculation as an immutable snapshot with its schedule — origination plus each re-term or prepayment capital change — so the current plan and every superseded one are auditable together.

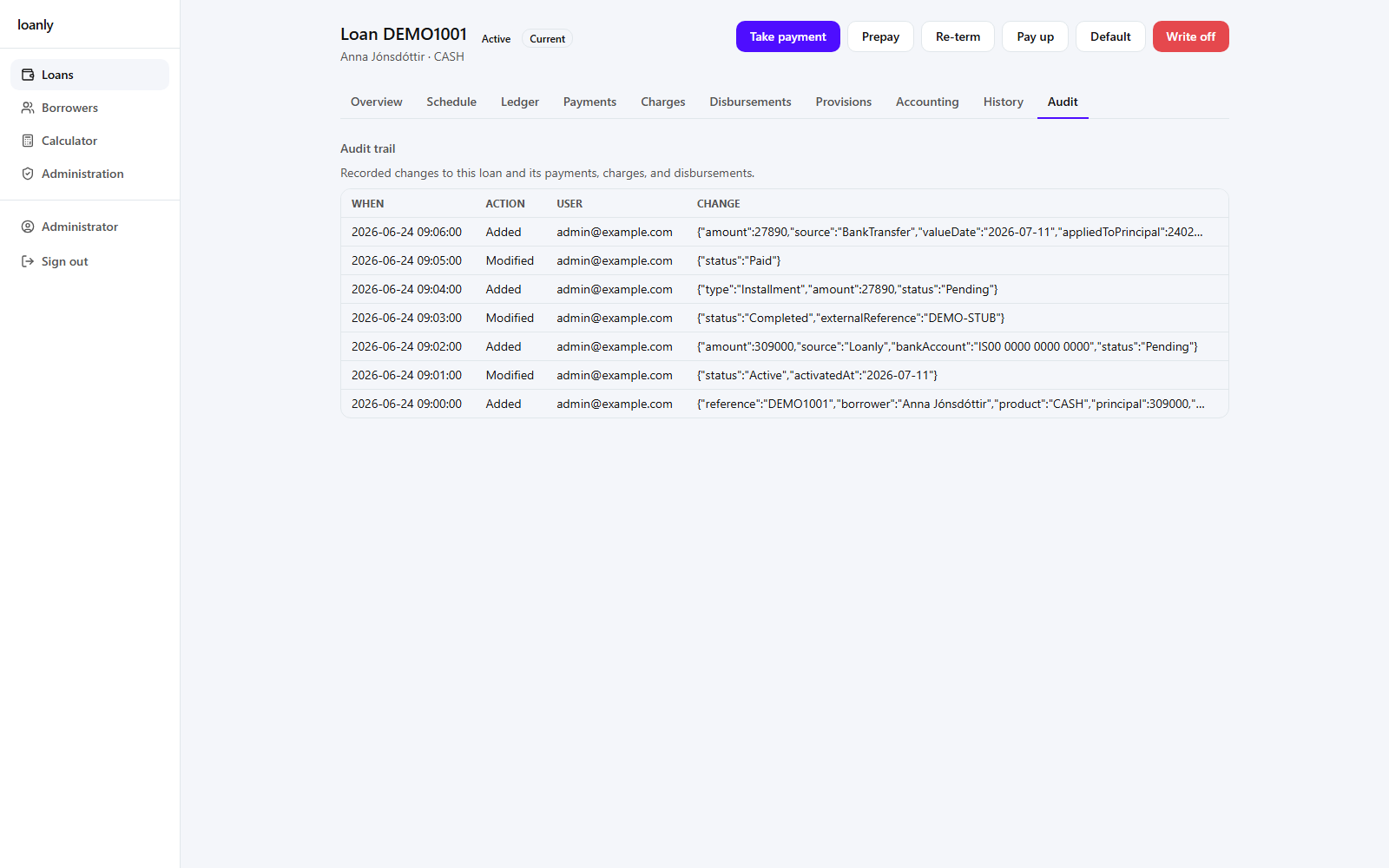

Audit

Every change recorded against the loan and its related records — the action, who did it, and when.

For how the lifecycle fits together, see Concepts → Loan lifecycle.